Recent perception of Short Term & Payday UK lenders

As opined by Barth et al. (2015) the present scenario in the UK regarding payday loans shows an increasing demand for reforming the policies and development to ensure a healthy deal to the customers. However, there is a lack of concrete evidence to base the policy guidelines from the perspective of the borrowers regarding short term & payday loans. This is the reason for researching the common market for payday loans. The information obtained will help in identifying the associated benefits and risks regarding payday loans and its present perception of the UK consumers.

The economic recession has resulted in a rapid growth of payday loans demand. The demand is mostly observed among the financially weaker sections as they are drained of all finances during the recession. The lack of availability of properly secured loans and consumers’ reluctance in purchasing long-term loans has led to the demand of the short term & payday loans.

Based on research conducted by Bhutta et al. (2015) the average loan estimated to £300. The research also highlighted that almost 1.3 million UK consumers took these payday loans in the year 2010. The research estimates total lending of 4 million loans amounting up to £1.4 billion. This resulted in a massive turnover for the payday loan industries amounting to £244 million in 2010 alone.

However, in the later years, the payday loans market has witnessed a significant growth with the advent of online loan procurement. Comparing with the average loan of £110 back in 2006, the average increased to £300 in 2010. This has been made possible due to the advent of online loans.

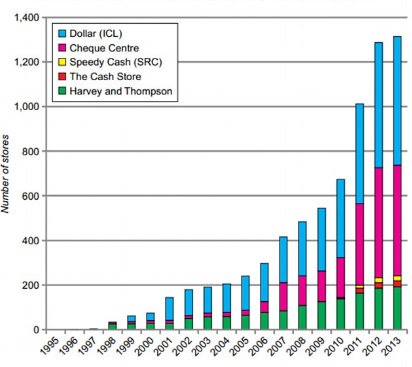

There has been an increase in loan procurement from 14% in FY 2009 to 21% in FY 2010 (Carter, 2015). These online loan providers tend to work on high costs, therefore, charging more on average than offline loan providers. The payday loan lenders work with significantly higher fixed costs for generating more profits. The profits incurred by these online providers have been significantly higher than those of the offline providers. Research conducted recently, suggests that the demand for payday loans continued to increase in the later years. It was expected to rise by 41-46% in the upcoming years. [Referred to as Appendix 1]

Appendix 1: Shows number of payday lending stores in the UK

Source: https://www.thisismoney.co.uk]

As per research conducted, the average UK household without any payday loans is absent. This is due to the requirement for all the borrowers in the UK to have at least one. The economic condition of the UK consumers though deteriorated after the recession hit yet they have better stability than their US counterparts. This has resulted in the demand for short term payday loans rather than long-term ones.

The emergence of young nuclear families has also lead to the demand for short term loans. However, there have been cases of difficulty among the UK borrowers. It has been estimated that in the UK almost 35% of loans are not being repaid under the initial agreement.

Awareness of UK consumers regarding new rules in 2014

According to Horton, (2017), after the new reforms came into action in 2014, the payday lending scenario in the UK witnessed a significant turn of events. The UK providers engaged in payday lending or other providing short term credit loans witnessed a significant fall. The price capping proved to be a reliable measure in protecting the borrowers. The consumers were made aware of the fact of not paying more than double the amount on the original borrowing. Media took an active role in spreading the awareness regarding new reforms.

As per the research conducted by the FCA, the people of UK were aware of the new reform policies, and they backed the changes. Clara, a school teacher in London, was quoted saying that she is confident of the new rules. Clara felt that new rules would create a balance between the consumers and the firms. Clara further states, that lowering the price cap would make the market viable. Clara furthermore added that placing a higher price cap results in insecurities among the borrowers.

A second survey conducted on a labour union showed people supporting this new change. A factory worker was quoted saying, that these new rules would protect those who struggle from repaying. The worker further backed this move by saying that most borrowers are often pressurised to repay their loans. This creates a pressure on the borrowers to repay it on time. Therefore putting a cap on the price would ensure substantial protection for the borrowers.

According to Howell, (2016), the UK consumers were made aware of the new bill passed from the Parliament through the active participation of the news media. The new bill stated that from the FY 2015, in the UK no borrowers would be subjected to pay back more than twice the amount borrowed. Therefore if a purchaser takes a loan of £100 then repayment, to the lender, would only amount to a maximum of £200.

However, it was also noted that the cap provided more transparent interest amounts which, in real terms, equate to a maximum of 292% Fixed APR, which means if you borrow £100 over 30 days and repay it on time and in full, you’ll pay back £124, which is £24 interest only.

As per a survey, in July 2014, it was estimated that around 11% of the total borrowers in the UK were made aware of the price cap and the repaying process. In the initial five months, the borrowing rate of loans dropped to 36% in FY 2015.

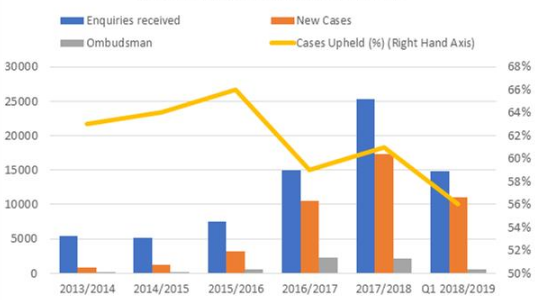

In more recent findings in 2016, an estimated 90% UK population were benefited from this policy. [Referred to as Appendix 2]

Appendix 2: Shows the payday loan complaints post 2014

Source: https://www.carnegieuktrust.org.uk/

In the first half of FY 2017, a further change in policies enabled the borrowers to take legal action against cases of duping or violating the rights of the borrowers. Under this new reform, over 5 million UK borrowers were safeguarded from overpaying their debts.

Change of perception of UK consumers

As mentioned earlier, the short-term payday market showed significant boom between the years 2006 to 2013. However, the new regulation policies under the reform policies of 2014, exhibited a fall of 40% in market loan volume. As per the study conducted by FCA, the market for short-term credit loans continued to fall drastically in the latter part of 2015. This fall in demand was however related to fall in demand. This fall in demand was later marked by an increase in loan purchases due to enhanced security and affordability. This trend continued until the fall of 2016 where the average loan size was relatively stable (opensecrets.org, 2018). Simultaneously, the price cap barrier of 2015 with the new regulations of 2014 minimised the problems of loan repayment among the economically weaker sections to a great extent.

The consumers with higher income brackets started buying long term loans. The credibility of the short term loans started decreasing from the latter half of 2015 and continued to fall in 2016. The consumers’ perceptions in affordability increased and the myth of short term credit affordability fell. By 2016, 56% of UK consumers agreed to purchase long term loans for its long term affordability. Almost 43% agreed that short term loan facility was a ‘saviour in disguise’. The economic viability that a long term loan possesses is more beneficial.

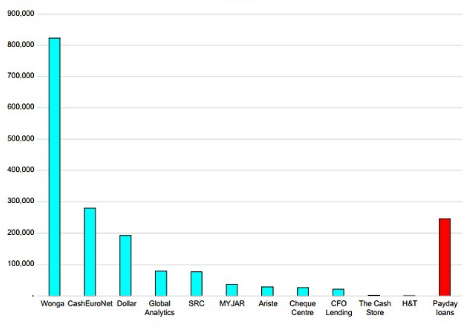

Only a staggering 26% of UK consumers did not agree with the new trend. Presently, 8 out of 10 customers in the UK consider long term credit loans are less easy, but the prospects are indeed huge. The most significant event that happened post-2014 regulations is the fall of repaying debts. New reforms changed the way the consumers used to perceive things. The debt proportion showed a sharp decline from 16% back in 2013 to 8% in 2016 (debt.org, 2018). Now, only 27% believes that they have profited from short term credit loans. [Referred to as Appendix 3]

Appendix 3: Shows payday loans concerning other loans

Source: https://www.thisismoney.co.uk/

Only 37% of them who would have borrowed short term payday loans are now seeking alternative measures. The awareness program created a sense of just among the UK citizens. Presently, only a mere 6% thinks of using unfair means of lending to procure short term credit loans. The transparency and efficiency of the lending system also improved. Only 16% of UK consumers were deprived of loans in 2016.

The rest were satisfied with the borrowing & lending process. The change in customers’ perceptions showed a direct impact on the loan industry. According to Khansalar et al. (2015), the average daily loans fell from 1.5% in 2013 to 0.7% in 2014. The consumers are paying relatively less for loans compared to the past. In light of the price capping, the average loan cost fell by 0.9% in 2015 followed by a 0.7% fall in 2016.

These new rules enabled the customers to be charged less for additional fees. This over time interest rate fell from 24% in 2013 to 13% in 2016. Surveys suggest that the amount of loans has significantly decreased up to 46% from FY 2013 to 2016 financial year.

Alternative measures in case of payday lender removal

Critics suggested in cases of removal of payday lenders, and the consumers would lack in borrowing options. However, this borrowing problem would only arise in procuring loans from payday lenders. Moreover, the new reform policies have opened up new prospects in borrowing facilities by implementing new measures. This has mostly benefited the lower income group and also those with higher income bracket in no small extent.

The alternative measures are listed below:

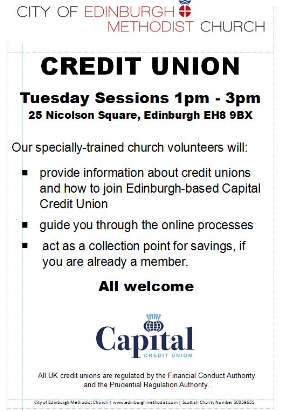

The Churches of England

The churches in England have lent an active voice in criticising the payday loans. It announced extensive plans of developing their credit line-up by collaborating with the other churches. The archbishop declared the abolishment of payday loans and fostered the setting up of a credit union. However, after an initial setback, the mutual credit union of the churches was set up, and it partnered with the Church of Scotland. Although initially, the churches mainly provided loans to the employees, trustees, and ministers of the church, however, later on, it was opened to the public. According to Lee and Brierley, (2017) the church union has made massive plans of expansion of lending facilities in the coming future. The UK citizens are made aware of these benefits through church programs, church pamphlets, and weekend masses. [Referred to as Appendix 4]

Appendix 4: Shows a credit union pamphlet of Edinburgh Methodist church

Source: https://www.grantonchurch.org.uk/

Post Office Banking

The British Parliament launched a series of new banking services and encouraged private entities to follow the same. This new business line uses post-office banking outlets to provide loans to customers. This move from the British government provided modern banking and loan services through post offices. However, Redmond, (2015) criticised this popular method by arguing this only benefited people of no bank accounts.

Furthermore, they stated that this only improved the condition of the lower income groups who rely on alternative lending services. The citizens of UK are made aware of this scheme by informing them via nationalised banks. The customers who possess a bank account in any of the nationalised banks of England are eligible for this loan scheme. Furthermore, the British government instructed the private banking institutes to follow this model due to its viability. It went a step further by providing loan incentives to draw customers from all economic strata of society.

Micro-loans

A new form of lending micro-loans started recently in the UK. This concept of micro-loans provided small amount loans for a brief period. This also served as an emergency loan for the UK citizens. This is a direct alternative to counter the short term payday loans by providing better affordability and marginal penalty in case of running debts. This new innovative program is gaining popularity in the UK from the assistance of labour unions (Rowlingson et al. 2016). Mostly, this scheme is popular among factory workers for its affordability and economic viability.

Reference List

Journals

Barth, J.R., Hilliard, J. and Jahera, J.S., 2015. Banks and payday lenders: friends or foes?. International Advances in Economic Research, 21(2), pp.139-153.

Bhutta, N., Skiba, P.M. and Tobacman, J., 2015. Payday loan choices and consequences. Journal of Money, Credit and Banking, 47(2-3), pp.223-260.

Carter, S.P., 2015. Payday loan and pawnshop usage: the impact of allowing payday loan rollovers. Journal of Consumer Affairs, 49(2), pp.436-456.

Horton, J., 2017. Young people and debt: getting on with austerities. Area, 49(3), pp.280-287.

Howell, N.J., 2016. Small amount credit contracts and payday loans: The complementarity of price regulation and responsible lending regulation. Alternative Law Journal, 41(3), pp.174-178.

Khansalar, E., Turner, N. and Giannopoulos, G., 2015. Perceptions of Regulation on the UK Mortgage Market: A Step Too Far?. International Journal of Business and Management, 10(8), pp.59-72.

Lee, B. and Brierley, J., 2017. UK government policy, credit unions, and payday loans. International Journal of Public Administration, 40(4), pp.348-360.

Redmond, W., 2015. The provisioning of inequality. Journal of Economic Issues, 49(2), pp.527-534.

Rowlingson, K., Appleyard, L. and Gardner, J., 2016. Payday lending in the UK: the regul (aris) ation of a necessary evil?. Journal of social policy, 45(3), pp.527-543.

Websites

debt.org, (2018) Payday Lenders and Loans Available at: https://www.debt.org/credit/payday-lenders/ [Accessed on: 14.12.2018]

opensecrets.org, (2018) Payday Lenders Available at: https://www.opensecrets.org/industries/indus.php?ind=F1420 [Accessed on: 12.12.2018]

paydayloaninfo.org, (2018) How Payday Loans Work Available at: https://paydayloaninfo.org/facts [Accessed on: 13.12.2018]